Why Almost Everyone Was Wrong About the Bitcoin ‘Halving’

May 11, 2024 12:00 AM UTC

4 derivatives

Bitcoin was falling Thursday and other cryptocurrencies were mixed, with momentum still lacking following a surge in prices earlier this year.

Bitcoin has fallen 0.7% over the last 24 hours to $62,106. The largest cryptocurrency, Bitcoin hit a record high near $74,000 in mid-March amid a surge of interest from new spot Bitcoin exchange-traded funds, or ETFs, but its price has since dropped.

On the face of it, the drop is puzzling, considering that the price should have been supported by the April 19 halving, when Bitcoin’s programmatic monetary policy changed—and the issuance of new tokens in half was cut in half, restricting supply.

One possible reason, according to J.P. Morgan strategist Nikolaos Panigirtzoglou, is that the halving was already priced in. J.P. Morgan analysts already saw Bitcoin as well above their volatility-adjusted comparison to gold, which would imply prices a $45,000 price.

A more bullish explanation could be that previous Bitcoin halvings have led to a more delayed cycle of price rises.

”The recent halving event has led to short-term downward price movements, a pattern observed in previous occurrences. Following this, there is typically a 9–12-month period of upward momentum, leading to the peak of the market cycle,” wrote Matteo Greco, research analyst at Fineqia International, in a recent research note.

Beyond Bitcoin, Ether—the second-largest crypto—was off 0.1% to $3,008.75. The Securities and Exchange Commission is expected to make a final decision on Ether spot ETFs this month. Optimism, however, has been muted for a quick follow-up to the approval of Bitcoin ETFs which sent Bitcoin to all-time highs.

“Market participants anticipate that the SEC will likely withhold approval for these products, despite approving BTC ETFs in January. Concerns over the liquidity of ETH’s spot and futures markets, along with its past classification as a security by the SEC, contribute to the skepticism surrounding swift approval,” wrote Fineqia’s Greco.

Smaller cryptos or altcoins were mixed Thursday, with Cardano down 0.8% and Polygon off 0.5%%, while Dogecoin had dipped 0.1%.

Gasoline prices increased this week to hover above last year’s average amid rising oil prices, falling inventories, and a more expensive summer blend of gas. The national gas average on Friday sat at $3.53 per gallon, nearly $0.10 higher than a year ago, according to AAA data. “Gas prices are a lot like seasonal temperatures. […]

Gasoline prices increased this week to hover above last year's average amid rising oil prices, falling inventories, and a more expensive summer blend of gas.

The national gas average on Friday sat at $3.53 per gallon, nearly $0.10 higher than a year ago, according to AAA data.

“Gas prices are a lot like seasonal temperatures. They start to rise with the arrival of spring," said Andrew Gross, a spokesperson for AAA.

The national average on Friday sat at a higher levelthan a year ago for the first time since late December.

Prices in California, the most expensive state for gasoline, approached $4.97 per gallon, $0.14 more the same day last year.

Gasoline prices typically rise heading into the spring as more motorists get on the road and refineries introduce a more expensive summer driving fuel blend. This year's retail prices have also been impacted by a steady climb in crude oil futures.

As of Friday, West Texas Intermediate (CL=F) contracts were hovering around $81 per barrel while Brent (BZ=F), the international benchmark price, traded near the $85 level. Brent and WTI have gained about $10 per barrel since the start of the year.

Ongoing output cuts from oil alliance OPEC+ along with Russian refinery interruptions stemming from Ukrainian drone attacks have lifted crude prices in recent weeks.

"While inventories are shrinking, most traders feel the latest rally in prices has happened a bit too far too fast and a corrective phase is needed. Still, the decline in Russia’s global exports (due to Ukrainian attacks) will be a supply factor as driving season begins, " Dennis Kissler, senior vice president at BOK Financial, said in a recent note.

The overview USD/JPY sits in a narrow trading range, sandwiched by bullish fundamentals and threat of intervention from the Bank of Japan to support the yen. The latter has reduced the odds of near-term upside for USD/JPY despite the release of important inflation updates in the United States this week. Unless the Japanese government softens […]

USD/JPY continued to sideways range trade, with bullish fundamentals offset by the threat of BOJ intervention

US CPI and PPI reports, the ECB interest rate decision and geopolitics loom as the key drivers for USD/JPY this week

Near-term bias remains to sell rallies in USD/JPY rather than buying dips

The overview

USD/JPY sits in a narrow trading range, sandwiched by bullish fundamentals and threat of intervention from the Bank of Japan to support the yen. The latter has reduced the odds of near-term upside for USD/JPY despite the release of important inflation updates in the United States this week.

Unless the Japanese government softens its public stance towards weakness in the yen, the preference is to sell rallies rather than buy dips or breaks. Geopolitical tensions in the Middle East are another wildcard for traders to navigate.

Key events for USD/JPY

There’s no need to reinvent the wheel when it comes to the likely USD/JPY drivers this week with the US interest rate outlook and geopolitics the key areas to focus on. As the latter is impossible to predict, what we as traders can do is look at the events that are likely to have the largest impact, taking into consideration positioning and technical factors.

Over the week, three such events stand out: the US consumer price inflation report on Wednesday, the US Producer price inflation report on Thursday and the ECB interest rate decision, also on Thursday. While the Fed speaking calendar is extremely busy, they key point to remember is the tone will be heavily influenced by these events, along with last Friday’s blockbuster US non-farm payrolls report.

There’ll be plenty of headlines to navigate, including from the FOMC minutes on Wednesday, but the vast majority will be noise and not impact USD/JPY meaningfully.

US CPI preview

Having topped market expectations at the headline and underlying level in the first two months of the year, markets may receive greater clarity as to whether the inflation acceleration is the start of a new trend or simply a seasonal anomaly.

Both headline and core CPI are forecast to lift 0.3%, down a tenth from February. While a deceleration, both would be incompatible with inflation returning to the Fed’s 2% inflation mandate in a timely manner.

The core services ex-housing figure, known simply as “supercore” inflation, will be influential given the Fed has nominated it as something it’s watching. It decelerated noticeably in February, minimising the damage to the dovish rates case despite the heat in other readings.

Potential USD/JPY market reactions

If that happens and we see no upside surprise in the core or headline inflation rates, it’s likely US front-end bond yields will decline, dragging back-end rates lower with it. That should narrow the yield differential between the US and Japan and weigh on USD/JPY. However, if we see another upside surprise, especially at the core level, USD/JPY and yields would likely lift, reflecting the diminishing case for Fed rate cuts in 2024.

Source: Refinitiv

US PPI, ECB rates decision in focus

The same approach applies for Thursday’s producer price inflation report with a hotter reading likely to lift USD/JPY, and vice versus if cold. A 0.3% gain is expected.

The ECB monetary policy meeting is the other key event simply because the euro is the largest weight in the US dollar index, making its fluctuations influential on other G10 FX names, including the yen. While no change in policy rates is expected, there is a growing risk it may signal the likely timing of its first rate cut will be brought forward from June. If that eventuates, EUR would likely weaken against the USD, dragging JPY along with it.

As for geopolitics, the rule of thumb is that if the tensions in the Middle East are subsiding, it should boost USD/JPY. If they escalate significantly, the likely repatriation of capital to Japan would weigh heavily on USD/JPY.

USD/JPY technical setup

With markets continued to pare rate cut expectations from the Fed, widening interest rate differentials with Japan, fundamentals suggest the bias for USD/JPY should be higher heading into the US inflation reports this week. However, with the threat of intervention from the BOJ elevated, rallies continue to suffocate on pushes towards resistance at 152, creating what I’ve described previously as a stalemate scenario.

With USD/JPY sandwiched by the intervention threat and bullish fundamentals, I’ll direct you to recent trade ideas that remain valid and have already worked since written. They can be accessed here and here.

The one overriding message is that while the technical picture looks bullish for USD/JPY, with a break of 152 pointing to the potential for substantial gains, the threat of BOJ intervention has greatly reduced the odds we’ll see significant upside should a topside break occur.

That suggests there’s limited reward and ample risk of going long on pushes toward 152. If the BOJ were to intervene, or even just signal such a move was imminent, USD/JPY could fall hundreds of pips in the space of seconds. As such, unless the Japanese government’s stance towards the weaker yen shifts substantially, selling rallies, rather than buying dips or breaks, remains the preferred strategy.

Resistance is located just below 152 with support located at 151.50, 151.20, 150.80 and 150.27. A more pronounced support zone is located between 149.58 and 149.00. Good luck!

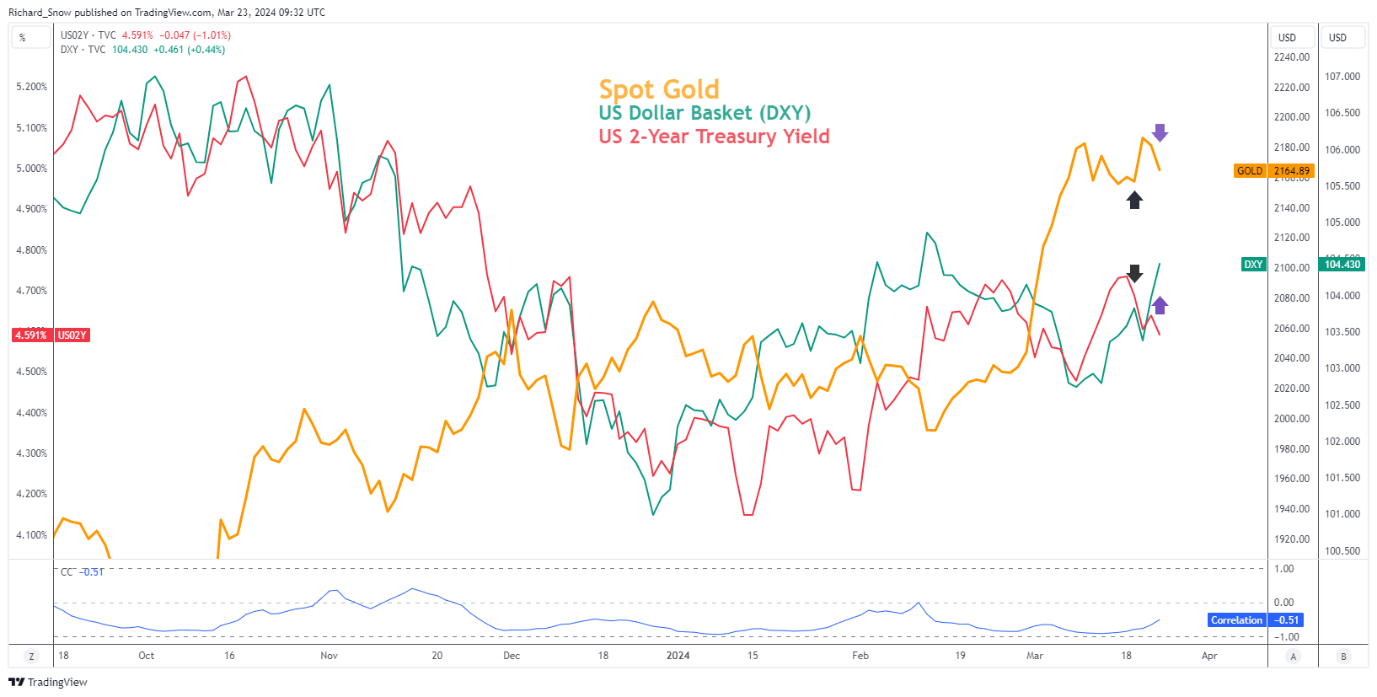

GVZ, or the gold volatility index, witnessed a strong move higher on Thursday as markets digested the recent Fed statement and latest summary of economic projections. The projections invalidated a growing belief in the market that the Fed will be forced to forgo a third rate cut in 2024 due to robust US data and resulted in a […]

GVZ, or the gold volatility index, witnessed a strong move higher on Thursday as markets digested the recent Fed statement and latest summary of economic projections. The projections invalidated a growing belief in the market that the Fed will be forced to forgo a third rate cut in 2024 due to robust US data and resulted in a dovish repricing in the dollar.

However, it has not taken long for markets to rally behind the dollar once again – something that is likely to keep the greenback supported into Friday’s PCE data which falls on Good Friday.

The chart below reveals gold’s recent responsiveness to the dollar (DXY) and shorter-term yields like the US 2-year yield. The aggressive move higher corresponded with falling yields and a lower USD but shortly thereafter,

Daily Gold Chart with DXY and 2-Year US Treasury Yields

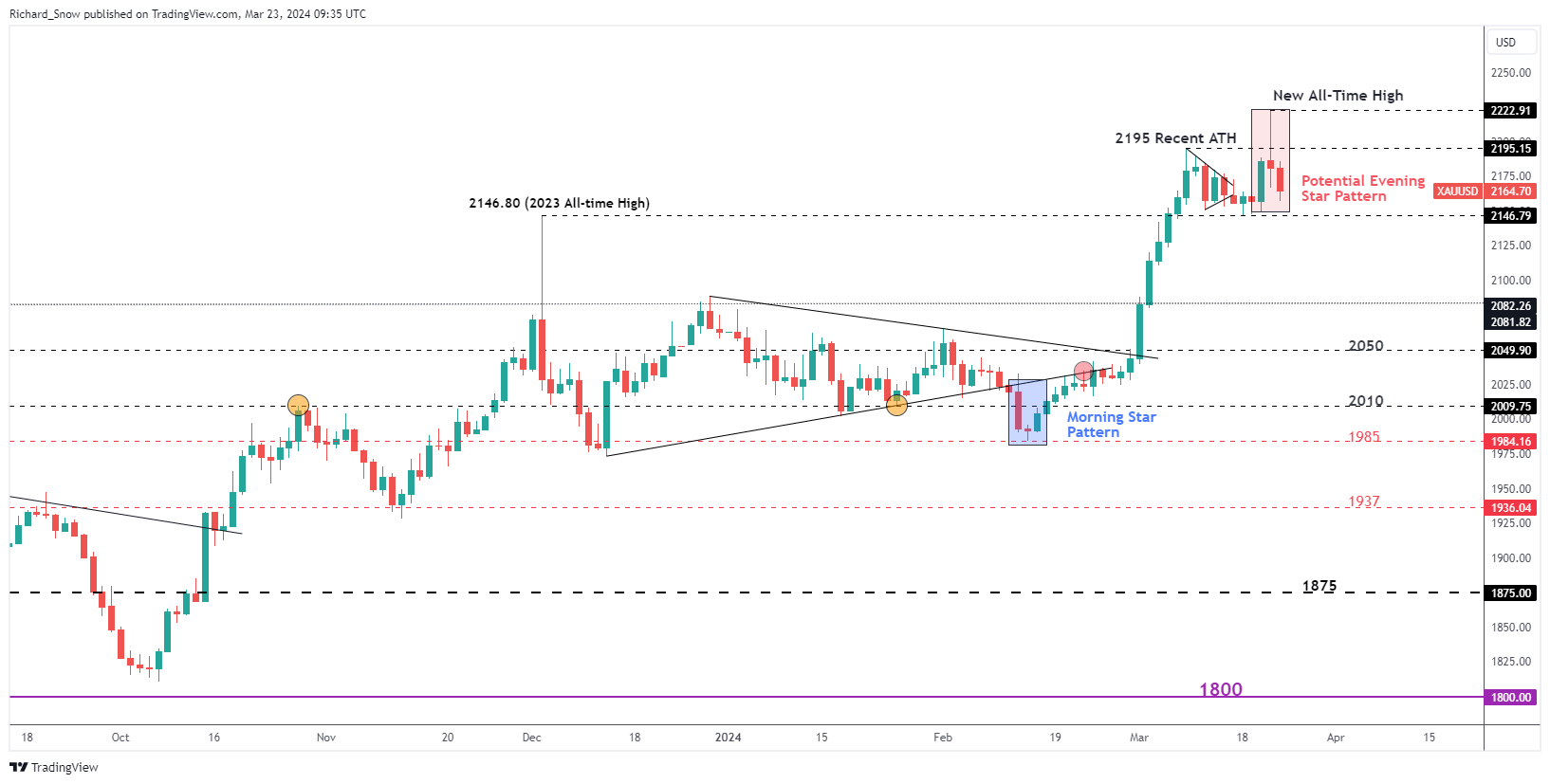

POTENTIAL EVENING STAR EMERGES MOMENTS AFTER PRINTING THE NEW ALL-TIME HIGH

An evening star could be emerging as the week came to a close, although the middle candle has a very notable upper wick which is not synonymous with the candle stick pattern. Nevertheless, price action suggests the recent move higher was an overreaction to the Fed news, as prices continued to ease into the weekend.

At the start of the coming week, the prior high of $2146.80 comes immediately into view as an early indication of whether bears may set the tone for the week. It’s a quiet week apart from final Q4 GDP data for the US and UK just to list a few and then on Friday PCE data for the month of Feb is due.

The dollars strong, immediate recovery poses a challenge for further upside for gold over the shorter-term and with few catalysts to choses from next week, gold may consolidate around the prior all time high with a view to trade lower.

The weekly chart helps put golds multi-week advance into perspective. The week before the one that’s just passed revealed a bit of a slowdown in bullish momentum and the candle relating to the most recent trading week that’s just come to a close, reveals a rejection of higher prices.

TOKYO (Reuters) – Japan’s economy likely contracted an annualised 1.5% in the January-March quarter as all key drivers of growth slumped due to an uncertain outlook, a Reuters poll showed, which will probably set back Bank of Japan efforts to raise interest rates. Cabinet Office data due out at 8:50 a.m. on May 16 (2350 […]

TOKYO (Reuters) - Japan's economy likely contracted an annualised 1.5% in the January-March quarter as all key drivers of growth slumped due to an uncertain outlook, a Reuters poll showed, which will probably set back Bank of Japan efforts to raise interest rates.

Cabinet Office data due out at 8:50 a.m. on May 16 (2350 GMT on May 15) is expected to show the economy's contraction would be equivalent to quarterly decline of 0.4%, according to the poll of 17 economists.

The decline followed growth of 0.4% annualised in the last three months of 2023, with the main pillars of GDP collapsing and leaving no growth engine for the January-March quarter.

"The trend of thrifty consumers remains strong due to rising living costs likely being exacerbated by the yen weakening," said Takeshi Minami, chief economist at Norinchukin Research Institute, who predicted the overall economy would contract at 1.2% annualised in the January-March period.

Private consumption, which makes up more than 50% of the economy, likely fell 0.2% in the quarter as consumers tightened belts to guard against the rising costs living.

The earthquakes that struck the Noto peninsula at the start of this year also undermined output and consumption. As well, a scandal at Toyota's compact car unit Daihatsu led to the suspension of output and shipments.

Capital expenditures also fell 0.7% quarter-on-quarter as companies remained slow to invest their hefty profits in plants and equipment, such as labour-saving technology to overcome labour shortages.

External demand, or net exports, which means shipments minus imports, likely shaved 0.3 percentage points off GDP growth. Domestic demand probably fell for a fourth straight quarter.

The corporate goods price index, a key gauge of prices corporations charge against each other, probably rose 0.8% in April year-on-year, keeping the pace unchanged from March.

The CGPI data will be released at 8:50 a.m. on May 14 (2350 GMT on May 13).

The CGPI, broadly equivalent to wholesale prices, likely rose 0.3% month-on-month in April, accelerating slightly from the 0.2% rise for March, underscoring persistent inflation that is boosting the costs of living and doing business.

(This story has been refiled to say quarterly decline, not monthly, in paragraph 2)

(Reporting by Tetsushi Kajimoto; Editing by Tom Hogue)

President Biden wants to raise taxes on Elon Musk, Jeff Bezos, and their cohort of Americans, who are amassing extraordinary wealth that is not taxable under current law. Biden says his plan would make the system more fair — but experts say it lacks practicality. The president wants to impose a minimum 25% tax on all Americans […]

President Biden wants to raise taxes on Elon Musk, Jeff Bezos, and their cohort of Americans, who are amassing extraordinary wealth that is not taxable under current law.

Biden says his plan would make the system more fair — but experts say it lacks practicality.

The idea of levying higher taxes on those at the top of the economic ladder is not new. Yet the latest proposal raises more questions than answers.

“Are you taxing the rich? Are you taxing the wealthy?” Peter Ferrigno, director of tax service at Henley & Partners, a citizenship investment consulting firm, told Yahoo Finance. “They're very similar, but they are not the same thing.”

Furthermore, the proposed policy challenges a fundamental principle of the US tax code, which treats money earned as income differently from wealth generated through valuation growth.

How could the US government tax wealth?

Biden hasn’t offered many specifics, but to get to a minimum 25% rate, experts say he would have to tax unrealized gains — unsold profits from increases in asset values — as part of billionaires’ income. Under current law, unrealized gains aren’t taxed until the asset is sold at a profit.

The president says this is the proper way to calculate the true income — and true tax rate — of the ultra-wealthy. Billionaires make the bulk of their money through stock or investment growth instead of a wage from a 9-to-5 job. So, the president says, they shouldn’t be able to shelter income simply because they haven’t pocketed the profits.

“Billionaires don't often have a typical paycheck,” Brandon Zureick, managing director and portfolio manager at Johnson Investment Counsel, told Yahoo Finance.

Take one of the world’s wealthiest people, for example: Elon Musk's net worth surged nearly $12 billion over a span of five years beginning in 2018, from $8.4 billion to $20 billion. However, Musk reported only $1.52 billion in income during those years and paid $455 million in taxes.

The 25 wealthiest Americans paid $13.6 billion in federal income taxes from 2014 to 2018. Meanwhile their wealth collectively increased by $401 billion in that same period, ProPublica reported. This means their collective average true tax rate was 3.4%.

To redesign this aspect of the tax code, Biden needs to consider: What happens when unrealized gains turn into losses?

In other words, how will the taxes work when investment values decline on paper?

“When you start taxing unrealized gains rather than realized gains, you're going down a very slippery slope,” Ferrigno said. “You want to tax the going up? Are you going to give money back when they go down again?”

For instance, if Musk’s share in Tesla (TSLA) surges from $100 billion to $200 billion, Biden’s proposed wealth tax would cost Musk $25 billion in that year — 25% of the unrealized $100 billion gain. But if Tesla shares declined by $100 billion the next year, would the government need to pay Musk back?

“That's where you open up a whole reason that other countries don't do this,” Ferrigno said. “Income tax has been around for centuries. And the reason no one's ever done this is because it's practically impractical.”

Democratic Rep. Alexandria Ocasio-Cortez wore a "tax the rich" dress at the 2021 Met Gala in New York City. (Photo by Jamie McCarthy/MG21/Getty Images for The Met Museum/Vogue ) (Jamie McCarthy/MG21 via Getty Images)

Top 1% pays nearly half of US tax

Opponents of a wealth tax reason that the share of federal taxes paid by the top 1% is already adequate. In 2021, the top 1% paid over $1 trillion, almost half of all tax revenue collected, according to the Tax Foundation.

“The income tax system in the United States is highly progressive and redistributive,” Erica York, senior economist at the right-leaning think tank Tax Foundation and author of its latest report on income tax data, told Yahoo Finance. The top 10%, she added, paid almost 76% of all tax revenue.

Critics also note that there is already a separate income tax on the rich, making Biden’s proposal redundant and unnecessary.

The alternative minimum tax (AMT) is a parallel system that sets a floor on what high-income individuals must pay. It removes some benefits and deductions on their tax returns, limiting the reductions to their tax liabilities.

“The US has had the alternative minimum tax for about 50 years,” Ferrigno said. “They already have a tool in the toolbox to try and address [taxes on high incomes].”

Ferrigno said an update to the AMT would be sufficient in taxing billionaires’ incomes.

A number of billionaires left Norway in 2022 after the country implemented a 1.1% capital asset tax. (Westend61 via Getty Images)

Caution: Don’t be like Norway

History shows how exorbitant income disparities can lead to social crises: “Back to the French Revolution and guillotine if not careful,” Ferrigno said.

But he said the Biden administration should start with a lower tax rate on billionaires, like 10%, and progress from there before landing at 25%.

After all, levying an overwhelming wealth tax on the super rich, who are also super mobile, can backfire. A number of billionaires left Norway in 2022 after the country implemented a 1.1% capital asset tax on married households with equity over the equivalent of $3.7 million.

“Find out what works and import it and avoid what Norway did to drive half of [ultra-wealthy] away,” Ferrigno said. “Look at how Spain has a high enough threshold that people just grudgingly accept it.”

Spain has a long-standing regional wealth tax from 0.16% to 3.5%. But instead of emigration, wealthy Spaniards either accepted their wealth tax rate or relocated to a cheaper region within the country.

“[Spain’s wealth tax] has been there for a long time as well, so people are used to it,” Ferrigno said. “Plus the exemptions ensure that few people get into the highest brackets.”

Switzerland also assesses various wealth taxes at the regional level on individuals’ assets worldwide, including bank account balances, equities, boats, and airplanes.

Transformative technology, such as blockchain ledgers and artificial intelligence, is transforming financial systems, yet the US tax codes haven’t kept up.

An overwhelming share of American voters, or 70%, support the idea of raising taxes on billionaires, a recent Bloomberg poll shows.

“Imagine what we can do,” Biden said of taxing the wealthiest Americans, “from cutting the deficit to providing for childcare, to providing healthcare, to continue to provide our military with all they need.”

“This is not beyond our capacity,” Biden said.

Rebecca Chen is a reporter for Yahoo Finance and previously worked as an investment tax certified public accountant (CPA).